Every fortnight, MutualFunds.com provides a snapshot of the performance of some key mutual funds which tries to accurately capture the investor interest in specific areas of the financial markets. The report is aimed at providing a quick overview of the sectors, regions and asset classes that moved in a meaningful manner during the last two weeks.

- Total long-term mutual funds saw net cash outflows of around $1.5 billion for the two weeks ended September 18, with equities seeing large net outflows. It was largely offset by positive net inflows in bond funds.

- Investors withdrew a net $17.2 billion from equity mutual funds during the two-week period, with domestic and large-cap equities seeing the largest outflows. Meanwhile, total bond funds saw $17.3 billion in net inflows, and hybrid mutual funds saw net outflows of around $1.6 billion.

- U.S. President Donald Trump faces the prospect of impeachment after Democratic House Speaker Nancy Pelosi launched a formal inquiry into the matter of Trump pressuring a foreign leader to investigate Joe Biden’s business dealings in the Ukraine for political gain. Biden, a former Democratic vice-president and a critic of Trump, is largely seen as having the biggest chance of winning the Democratic nomination for president in 2020.

- Germany’s ZEW economic sentiment improved from negative 44.1 to 22.5. Although an improvement, this was the fifth consecutive month of contraction.

- The U.S. Federal Reserve again cut interest rates to 2%, but some policymakers dissented on the decision. Two officials said the U.S. central bank should have kept interest rates unchanged at 2.25%, while a third one, James Bullard, believes the bank should have decreased rates by 0.5% to insure against further declines in inflation. Trump, who favors more aggressive rate cuts, criticized the Fed’s decision.

- The Bank of Japan has kept its monetary policy steady but signaled further easing in October as it fears a potential slowdown in the global economy. The central bank kept its overnight interest rates at minus 0.1% and its target for 10-year bond yields at zero percent.

- The Bank of England decided to keep interest rates unchanged at 0.75%, with the monetary policy committee unanimously voting for the move. However, the bank strongly hinted that it may cut interest rates due to Brexit uncertainty.

- Germany’s flash manufacturing purchasing managers’ index (PMI) declined to 41.4 from a record low of 43.5, the lowest level since June 2009, when the economy was recovering from the financial crisis. Meanwhile, Europe-wide manufacturing PMI declined to a nearly seven-year low of 45.6.

- U.S. core durable goods orders rose 0.5% in August compared to the previous month, beating expectations of 0.2% growth. Overall, goods orders increased by 0.2% versus a decline of 1.1% expected by analysts.

Broad Indices

- The performance of equities and bonds diverged over the past two weeks.

- The U.S. Nasdaq 100 fund (NASDX) saw the biggest decline, losing 2.7%.

- Meanwhile, Vanguard’s total bond market fund (VBMFX) gained 1.2%, the best performance from the pack.

Major Sectors

- Sectors were largely down.

- Vanguard’s telecommunication services sector fund (VTCAX) dropped more than 4% for the past two weeks, becoming the worst performer.

- At the same time, utilities sector fund (FKUTX) gained the most these past two weeks, up 3.3%, as investors favored safe-haven assets in the face of increasing macroeconomic and political uncertainty.

Foreign Funds

- Foreign funds posted widely disparate performances, with India by far the best performer and China on the other end of the spectrum.

- India equities fund (WIINX) surged nearly 8% after the country’s government decided to scrap a tax increase.

- Chinese equities fund (MICDX), meanwhile, declined nearly 5% for the past two weeks.

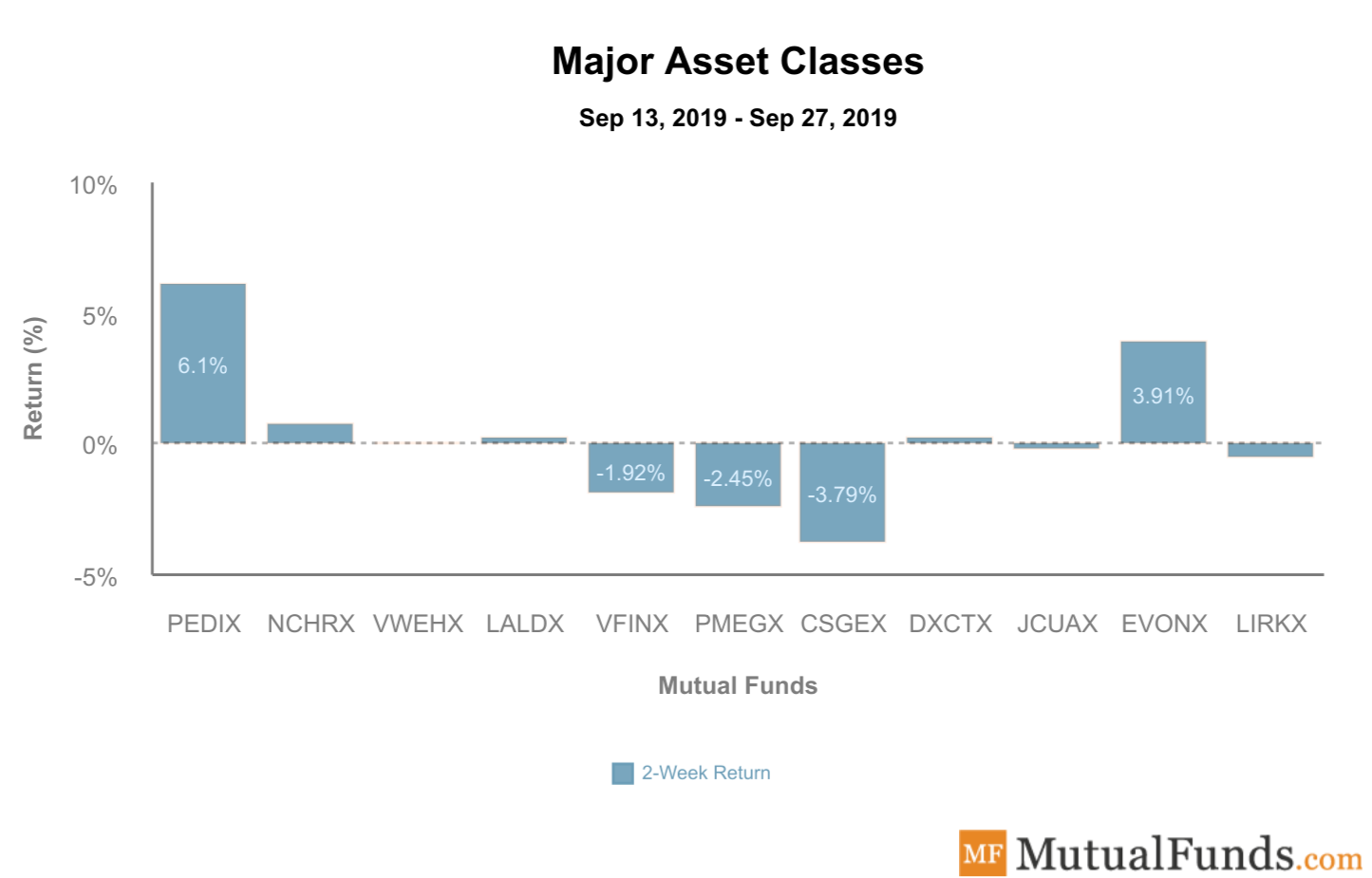

Major Asset Classes

- In asset classes, bonds and managed futures have outperformed equities, as investors flocked to safe-haven assets.

- PIMCO’s long-term bond fund (PEDIX) was the best performer from the pack with a gain of more than 6%.

- At the other end of the spectrum, BlackRock’s small-cap fund (CSGEX) lost 3.8%.

The Bottom Line

Net bond inflows were slightly offset by net equity and hybrid fund outflows, providing for an overall negative picture of mutual fund flows. Technology and telecom stocks were among the biggest losers these past two weeks, while long-term bonds and utilities were strong performers on the back of fears of an impending global economic slowdown. Meanwhile, Indian equities surged after the government scrapped a tax hike with the aim of boosting the stock market.

Be sure to sign up for your free newsletter here to receive the most relevant updates.